2. What is a lease under ASC 842?

4. Scope of ASC 842: What’s covered and what’s not covered?

5. ASC 842 subtopics: Lease types in scope

- Operating lease accounting under ASC 842 and examples

- Finance lease accounting under ASC 842 and examples

12. ASC 842 vs. IFRS 16: What are the differences between the two?

13. ASC 842 software: What are the benefits beyond compliance?

What is ASC 842?

ASC 842, or Topic 842, is the new lease accounting standard issued by the FASB and governs how entities record the financial impact of their lease agreements. Among other changes, it requires all public and private entities reporting under US GAAP to record the vast majority of their leases to the balance sheet. This new standard was established to enhance transparency into liabilities resulting from leasing arrangements and reduce off-balance sheet activities.

What is a lease under ASC 842?

ASC 842 defines leases as contracts, or portions of contracts, granting “control” of an identifiable asset for a specific period of time in exchange for payment. The term “control” carries a distinct meaning in this definition. To demonstrate control of an asset, a business entity must be able to obtain “substantially all” of the economic benefit from the asset’s use and direct its use throughout the period of the contract.

ASC 842 effective dates

Effective date of ASC 842 for public companies

Public and private companies have different effective dates for the new lease accounting standard. For public companies, the FASB standard was effective for reporting periods beginning subsequent to December 15, 2018. For calendar year-end companies, this means the standard was adopted on January 1, 2019.

Effective date of ASC 842 for private companies

ASC 842 is effective for the annual reporting periods of private companies and nonprofit organizations beginning after December 15, 2021. This means many private companies and non-profit organizations are working through the lease accounting transition for the 2022 year-end.

Scope of ASC 842: What’s covered and what’s not covered?

ASC 842 applies to most leases and subleases, but exceptions do exist. On occasion, a contract contains a lease, but it’s out of the scope of Topic 842 and the guidance should not be applied to the transaction. Here are the out-of-scope lease types, as detailed in Subtopic 842-10-15-1:

- Leases of intangible assets, such as cloud computing arrangements. The guidance for these agreements can be found in ASC 350, Intangibles – Goodwill and Other.

- Leases for the exploration or use of non-regenerative natural resources such as oil, natural gas, and minerals are covered under ASC 930, Extractive Activities – Mining, and ASC 932, Extractive Activities – Oil and Gas.

- Leases of biological assets such as plants, animals, and timber. These are addressed in ASC 905, Agriculture.

- Leases of inventory, which are covered under ASC 330, Inventory.

- Leases of assets that are under construction. These are addressed in ASC 360, Property, Plant, and Equipment.

ASC 842 subtopics: Lease types in scope

ASC 842 is made up of five subtopics – an overview and four sections covering the following transaction types:

- Lessee accounting for operating leases and finance leases

- Lessor accounting

- Sale-leaseback transactions

- Leveraged lease arrangements

Lessee accounting under ASC 842

Similar to ASC 840, the prior lease accounting standard, ASC 842 uses a two-model approach for lessees; each lease is classified as either a finance lease or an operating lease. This applies to all leased asset categories covered under the standard, including leases of equipment and real estate. “Finance lease” is a new term and replaces the term, “capital lease,” used under Topic 840. Additionally, ASC 842 changes the criteria defining a finance/capital lease.

Lessees reporting under Topic 842 are required to recognize both the assets and the liabilities arising from their leases. The lease liability is measured as the present value of lease payments, while the lease asset is equal to the lease liability adjusted for certain items like prepaid rent, initial direct costs, and lease incentives.

Among the many changes to lease accounting under this standard, the most significant is operating leases will be recorded on the balance sheet as lease assets and lease liabilities. The asset is known as the right-of-use asset, or ROU asset, and represents the lessee’s right to use the underlying asset while the lease liability represents the lessee’s financial obligation over the lease term. When measuring the assets and liabilities, both the lessee and the lessor should also include “reasonably certain” lease renewals beyond the current lease term and “reasonably certain” asset purchase options.

For leases with terms of 12 months or less, lessees can elect not to recognize lease assets and liabilities. They should instead recognize lease expense on a straight-line basis, generally, over the term of the lease, similar to the accounting treatment under ASC 840.

Existing capital leases will not require adjustment or remeasurement upon transition, but they will be referred to as finance leases.

Operating lease accounting under ASC 842 and examples

When accounting for an operating lease, the lessee must:

- Recognize a single lease cost allocated over the lease term, generally on a straight-line basis

- Classify all cash payments within operating activities on the statement of cash flows

For a full example of an operating lease beginning pre-transition and the accounting treatment at transition, read our article, “Operating Lease Accounting under ASC 842 Explained with a Full Example.”

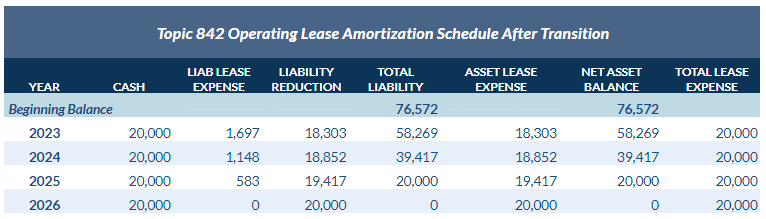

Below is an example of the accounting for an operating lease beginning post-transition. For the example, let’s assume the following facts:

- Payment terms: $20,000 annually

- Start Date: 1/1/2023

- End Date: 12/31/2026

- Incremental Borrowing Rate (IBR): 3%

- The lessee determines this is an operating lease

Based on these circumstances, the present value of 4 annual payments of $20,000, made in advance, with a 3% IBR is $76,572. The annual operating lease expense is $20,000, or the straight-line treatment of 4 annual payments with no escalations, rent holidays, etc. The amortization schedule for this lease is below.

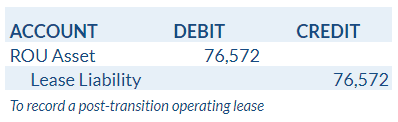

The entry to record the lease upon its commencement is a debit to ROU asset and a credit to lease liability:

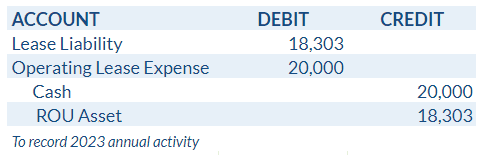

Subsequent entries follow the amounts set forth in the amortization table. The entry for the annual activity of 2023 is below.

Finance lease accounting under ASC 842 and examples

When accounting for finance leases, lessees must:

- Recognize interest on the lease liability and amortization of the ROU asset in separate line items of the income statement

- Classify payments of the principal portion of the lease liability within financing activities and payments of interest on the lease liability within operating activities on the statement of cash flows

Per the guidance, existing capital leases will not require adjustment or remeasurement upon transition, provided they were accounted for correctly under ASC 840. Therefore the accounting treatment of a capital/finance lease beginning pre-transition will be the same as the accounting required post-transition and no transition accounting adjustments will be necessary.

However, one exception is if any deferred or prepaid rents associated with the capital/finance lease exist at transition. Any remaining balances of deferred or prepaid rents become adjustments to the related ROU asset.

We’ve detailed a full example of a finance lease beginning post-transition in another article, “Capital Lease Accounting and Finance Lease Accounting: A Full Example.”

Download the Ultimate ASC 842 Guide for more examples

Our Ultimate Lease Accounting Guide for ASC 842 contains 44 pages of examples, journal entries, disclosures, and more step-by-step guidance on operating leases and finance leases under the new standard.

Lessor accounting under ASC 842

Lessor accounting remains largely unchanged from ASC 840 to 842. Lessors can classify leases as operating, sales-type, or direct financing leases, but the leveraged lease type under ASC 840 is eliminated under ASC 842. Lessor accounting is covered in full detail in ASC 842-30. No significant changes were made to the requirements for balance sheet recognition.

For operating leases, the leased asset will continue to be recognized as a fixed asset on the lessor’s books. Whereas for both sales-type and direct financing leases, the lessor derecognizes the underlying leased asset and records a net investment in the lease on the balance sheet. While income from operating leases is recognized on the income statement as rental income; when cash is received from sales-type and direct financing leases, a portion is applied as a reduction to the net investment in the lease, and a portion is recognized as interest income.

Read more about accounting for lessors in our article, “Lessee vs. Lessor: Differences, Accounting, & More Explained”

Sale-leaseback accounting under ASC 842

In a sale-leaseback transaction, the lessee sells the asset to the buyer/lessor and enters into an agreement to lease the asset back from the buyer/lessor. This type of transaction consists of both a sale and a lease. The determination of whether or not the transaction is a sale is performed in accordance with ASC 606, Revenue from Contracts with Customers.

As a result of the changes under both ASC 606 and ASC 842, some transactions not qualified for sale and leaseback accounting under ASC 840 will qualify under ASC 842. The opposite is also true: some sale-leaseback transactions under ASC 840 will no longer qualify for this accounting under ASC 842. However, transactions correctly accounted for using sale-leaseback accounting under ASC 840 do not have to be reassessed during the transition to ASC 842.

For a full example of a sale-leaseback transaction, read our article, “Sale-leaseback Accounting under ASC 606 and ASC 842 Explained.”

Leveraged lease accounting under ASC 842

Under Topic 840, a leveraged lease is defined as an agreement in which the lessor borrows funds from a lender to help pay for the purchase of an asset that is then leased to a lessee. The lender holds the title of the asset and the lease payments made by the lessee are collected by the lessor. The lessor is then responsible for sending payments to the lender.

As we mentioned above, ASC 842 essentially eliminates the leveraged lease classification. Lessors can only classify a lease arrangement as a leveraged lease if the commencement date is prior to the effective date of the new lease accounting standard. The accounting is detailed in ASC 842-50.

Ultimately, this means no new leveraged leases will be created following the final effective date of the new standard. Leases with a commencement date falling after an entity’s effective date for ASC 842 should be accounted for in accordance with the rules for lessor accounting (covered earlier in this article) contained in ASC 842-30.

ASC 842 practical expedients

Topic 842 offers elections meant to ease the transition process, referred to as practical expedients. Some of the practical expedients under ASC 842 include grandfathering of lease classification, combining lease and non-lease components, and not restating the prior year’s financials.

A more thorough explanation of the various practical expedients available can be found in our article “Practical Expedient in Accounting Explained: Adopting ASC 842 and IFRS 16 with Ease.”

ASC 842 disclosure requirements

ASC 842 requires both qualitative and quantitative disclosures. A few of the specific disclosures required are:

- Discussions covering the lease arrangements

- Descriptions of significant judgments made

- Details about the lease costs reported on the income statement

- Weighted-average analysis of discount rates and remaining lease terms

We provide a full overview of the disclosure requirements of ASC 842 with examples in our article, “ASC 842 Disclosure Requirements: Example and Explanation.”

ASC 842 vs. IFRS 16: What are the differences between the two?

Despite the Boards’ efforts to streamline lease accounting with the convergence of these new standards, some major differences between the two standards emerged. For example, ASC 842 continues to distinguish between finance and operating leases, both are now required to be recorded on the balance sheet. Alternatively, IFRS 16 removes the operating lease classification and requires that all lessee leases be treated as finance leases.

Here are a few more examples of how the two differ:

- Under IFRS 16, the lease liability is remeasured each time the reference index or a rate that variable lease payments are tied to resets, whereas ASC 842 does not require the lease liability to be remeasured when indices or rates are reset.

- Though FASB Topic 842 does not explicitly exclude immaterial leases or low-value assets, these are exempt from balance sheet recognition under IFRS 16. The Basis for Conclusions paragraph 100 to IFRS 16 addresses how companies can define “low value” assets and offers a threshold of $5,000 for consideration.

- FASB Topic 842 permits private companies to use a risk-free rate to calculate the lease liability, but IFRS 16 does not provide guidance specific to private entities.

- While FASB Topic 842 generally requires interest payments to be included within operating activities on the statement of cash flows, IFRS 16 allows interest to be reported within operating, investing, or financing activities.

For more examples of differences covered in full detail, read our article, “IFRS 16 vs. US GAAP Lease Accounting: What Are the Differences?”

ASC 842 software: What are the benefits beyond compliance?

There are numerous benefits to implementing software for ASC 842 lease accounting, such as LeaseQuery. Here are just a few:

1. More opportunities for lease management

One invaluable feature is getting alerts for critical dates related to your leases, such as reminders about renewals, payment changes, terminations, etc. These alerts can help you manage and track those critical dates better. Having the ability to build customized reporting for lease management purposes like tracking cost per square footage or annual payment information is also an important feature when evaluating software.

2. Improvements to accounting accuracy and reduction of errors

Many companies are still using Excel for lease accounting instead of using an accounting-focused software solution. Excel is more manual, takes more of the accounting team’s time, increases the effort needed to complete audits, and often leaves companies with doubts about the accuracy of their calculations.

Some companies even have horror stories about using Excel for leases. For example, using Excel for tracking leases resulted in a $648,000 overpayment of rent for one customer before their LeaseQuery implementation. The inability to set up an alert to notify the accounting department when periodic rent should have been abated on every anniversary of the lease led to multiple years of steep unnecessary payments.

Another company lost a tenant improvement allowance worth over $2 million after they realized the TIA was not transferred appropriately during an acquisition. Excel had nowhere to capture the information.

Finding software that assures controls and calculations can provide additional trust in the accuracy of your financials. An accounting software vendor needs to provide this assurance through SOC reports.

3. Modifications, renewals, and other day two accounting made easy

Even after the transition process, lease accounting challenges will still exist. These can include new leases, modifications, impairment, renewals, and even standard changes. This can also include organizational changes like mergers and acquisitions, new balance sheet and income statement accounts, training new staff, etc.

Having a software to maintain compliance and keep up with day two lease accounting can help your team be more efficient and have a smoother close process. For more details on day two lease accounting, see our article.

4. Improved budgeting and forecasting

The right software can provide the ability to budget or forecast the income statement, balance sheet, and cash flow impacts from lease accounting at transition as well as in a steady state. Budgeting and forecasting functionality allow you to identify how much cash you’ll spend in a given period as well as how much will be spent by a particular region, department, or business division.

Your solution’s out-of-the-box forecasting reports should be able to help determine the impact your lease portfolio has on important reporting metrics, such as earnings per share and EBITDA. Using anything other than lease accounting software to calculate the above would require quite a bit of extra effort.

Finding a lease accounting solution that has custom reporting features is also important so you can create a report specifically for your organization’s needs. That way, you’ll be an expert when colleagues request information about leases and their financial impact on the company.

5. Improved financial footnote disclosures

Without support from software, gathering the information for the quantitative lease disclosures can be a time-consuming task. After this data is gathered, the accuracy has to be validated for the auditors and internal control requirements. Having software that can provide the full set of quantitative disclosures out-of-box can allow your company to quickly aggregate the data to complete your financial footnote disclosures as detailed above.