Background

The coronavirus pandemic continues to impact global economies and local communities alike. Businesses across all industries and sizes are continuing to face challenges to their operations and, for some, adjusting to working remotely.

As companies monitor cash flow during the pandemic, they may be looking at any under-used assets and reviewing existing and upcoming lease commitments. Dealing with a legal battle over non-payment of rent is not an ideal situation for either party, especially during this already stressful time. Both parties may decide to renegotiate the lease terms. However, as a lease serves as a legally binding contract from the moment it is signed, the lessee and the lessor must agree on any changes to the lease terms.

Changes to lease payments under COVID-19

Businesses are attempting to renegotiate their lease agreements to find terms that are agreeable for both lessors and lessees in these challenging times. Some examples of possible rent concessions include rent forgiveness, rent reductions, or a rent “credit”. Another scenario is changing the timing of lease payments through a rent deferral, with payment or payments occurring at a later date.

The IASB (also known as the Board) has acknowledged that due to the implications of COVID-19, many lessors are providing rent concessions to lessees in a quantity never expected. Under IFRS 16, unless these concessions were contemplated in the agreement, any of these mentioned rent concessions may trigger a lease modification, as there has been a change in the terms and conditions of the contract. The Board realized that lessees would face challenges in evaluating and accounting for these lease concessions under the IFRS 16 modification framework.

IASB response

In response to concerns about the complications that changes in lease agreements due to COVID-19 pandemic would have on financial reporting, on May 28, 2020 the IASB provided a practical expedient to lessees in the form of an amendment to IFRS 16. This amendment is effective for annual reporting periods beginning on or after June 1, 2020. However, earlier application is permitted.

This practical expedient permits lessees to bypass the assessment of whether rent concessions that occur as a direct consequence of the COVID-19 pandemic are lease modifications. Instead, this expedient allows lessees to account for those rent concessions as if they were contemplated in the original contract, and therefore, are not lease modifications.

The IASB has provided this expedient as an optional election for lessees. If a lessee chooses to apply the expedient, the organization will need to apply it consistently to all lease contracts with similar characteristics in similar circumstances.

To further address questions around scope and applicability, the IASB also specified that this expedient is only applicable for lease concessions that are a direct result of the impact of COVID-19. It’s also important to note that any change to a lease agreement must be agreed upon by both parties. A change in the payments outlined in the lease agreement NOT agreed to by both the lessee and the lessor, such as “short-pays,” are not eligible for this election.

Additionally, the COVID-19 rent concessions must meet the following conditions:

- The change in the lease payments results in payments that are substantially the same as, or less than, the consideration for the lease immediately preceding the change. Substantially the same is not explicitly defined by the IASB, so judgment will need to be applied. Generally, using a 10 percent threshold is appropriate for determining what is considered substantially the same.

- The rent concession impacts lease payments that were originally due on or before June 30, 2021. If the concession leads to a reduction in lease payments that extends beyond June 30, 2021, the entire rent concession would not be within the scope of the IFRS 16 practical expedient. However, if the rent concession results in reduced payments on or before June 30, 2021, and a related increase in payments beyond June 30, 2021, this would not prevent the concession from being in scope.

- The rent concession introduces no other substantive change to the lease, either qualitatively or quantitatively. This accounting option is for payment related concessions only and does not allow a lessee to account for additional significant changes. For example, if the parties agree to defer the rental payments from June 2020 to be due in December 2020 or to a concession of 30% of the rental payment due for July 2020, the election can be applied. However, if rent concessions coincide with a significant increase in the lease term, (i.e. the concession’s impact is NOT substantially the same as the original lease payments) this must be recognized as a modification under IFRS 16. As another example, if the rent concessions also require the lessee to extend the lease term by three additional years, this concession would not be in scope for the IASB COVID-19 election. This is because, while payments in certain months may have decreased as a result of the rent concession, the total payments for the lease term have increased substantially with the addition of three years of payments.

Unlike the approach provided by the FASB, which you can read about here, the IASB only allows lessees to elect this optional relief treatment. It is not available for lessors.

Accounting for COVID-19 lease concessions

Below, we will describe two of the methods outlined in the IASB relief guidance that a lessee can use to account for COVID-19 rent concessions.

Rent Reductions

APPROACH: Negative variable lease payments

If a lessee and a lessor have agreed to a rent concession that involves a reduction of payments due to COVID-19, this accounting approach allows for the rent reduction to be treated by the lessee as a negative variable lease payment. The reduced payments are recorded as negative lease expense in the months the full amount of rent payment would have been due per the original lease agreement. Using this approach, there is no impact on the ROU asset, lease liability or the lessee’s amortization schedule.

As an example, let’s assume an original lease agreement has monthly payments of $5,000 and due to the impacts of COVID-19, a lessee and a lessor have agreed to reduce one month of lease payments to $3,000. Using this approach, the lessee would make the following journal entry in the month of rent reduction:

An advantage of using this approach is that the reduced cash payment is recognized in the current period, but there is no impact on the lessee’s total amortization schedule. The lease expense recognized will be lower in the periods in which a rent reduction has occurred. It is important to note that because the lease liability will continue to be reduced based on the existing amortization schedule (there is no impact or adjustment to the lease liability), the lease liability may not represent the company’s true legal obligation.

Rent Deferrals

APPROACH: Remeasurement consistent with resolving a contingency

As a result of COVID-19, lessees may reach an agreement with their lessor for a rent concession that involves a deferral of payments. The timing of the payments may be pushed out until a later date with no changes to the total consideration in the original lease and no change to the total cash flows over the lease term, resulting in a deferral of payments. The second approach allows the lessee to treat the payment reduction as an option the lessee is entitled to under the original lease contract. The new timing of the rent payments is accounted for as a resolution of the contingency that was specified in the original lease. Using this approach, the lessee remeasures the lease liability at the date of the concession, using the updated payment timing. However, unlike a lease modification, the lessee does not update the discount rate used in the lease. Additionally, the lessee will not reassess the lease term or any lessee purchase options.

After calculating the present value of the updated lease payments, the carrying value of the lease liability is adjusted to reflect the carrying value of the remeasured lease liability, and the lessee makes a corresponding adjustment to the ROU asset.

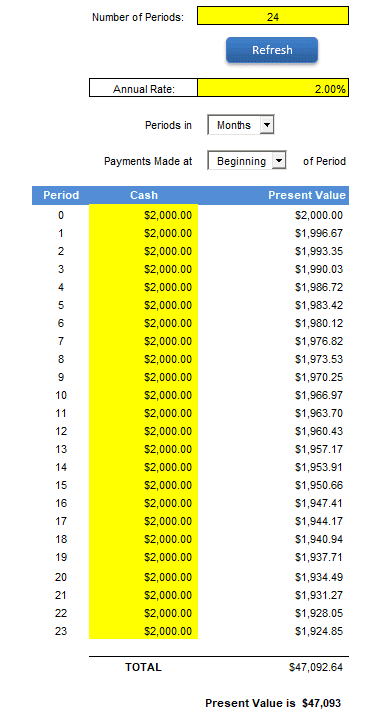

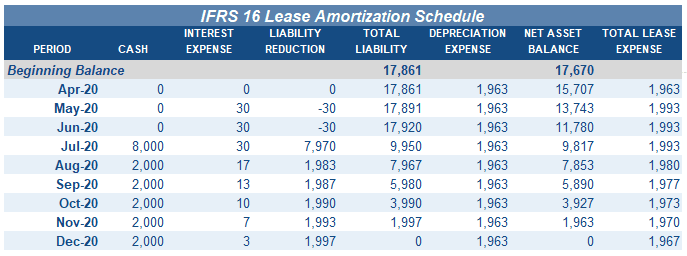

As an example, assume the lessee has an original two-year lease with $2,000 monthly payments made in advance each month. Assume an original discount rate of 2%

Using the present value calculator tool, the initial lease liability and ROU asset are $47,093.

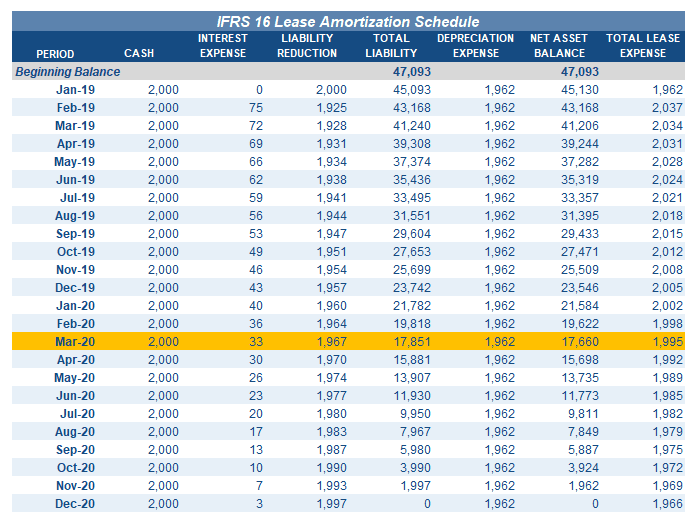

With the facts presented, the following is an example of the amortization table for this lease agreement:

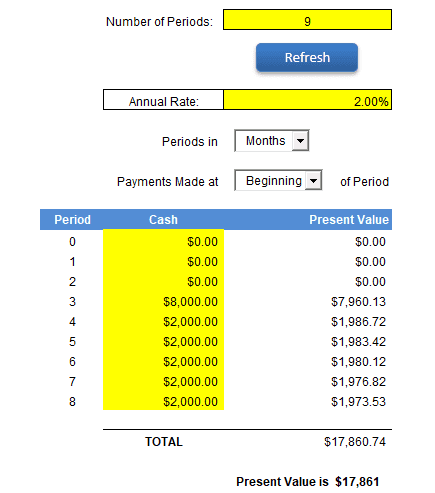

At the beginning of April 2020, the lessee and lessor agree to a concession as a result of COVID-19 to defer the lease payments for the months of April, May, and June. These payments are now due on July 1st (0 payments due in April, May, and June and $8,000 due in July). As shown in the table above, before the rent concession, the carrying value of the lease liability is $17,851 and the carrying value of the ROU asset is $17,660. To calculate the revised lease amounts after the rent deferral, a customer can use the present value calculator as of April 2020, the date of the rent concession, and remeasure the lease liability. The new remeasured lease liability as of April 2020 is $17,861.

The difference between the remeasured lease liability and the lease liability before the lease concessions were granted is an increase of $10 ($17,861 – $17,851). The increase is recorded as a credit to the lease liability, with a corresponding debit, or increase, to the ROU asset. This is done by the following entry:

After the adjusting entry to the lease liability and the corresponding ROU asset to record the remeasured value, the updated amortization table is as follows:

Disclosure Requirements

The IFRS 16 amendment requires lessees to disclose when the practical expedient election for rent concessions is elected. If it was not applied to all concessions, the lessee discloses to which specific types of contracts it was applied. Additionally, lessees should disclose the amount recognized in profit or loss for the reporting period to reflect changes in lease payments as a result of applying the practical expedient to account for COVID-19 rent concessions. The Board also recognizes that if a lessee chooses to elect the practical expedient, lessees may have non-cash adjustments to certain lease liabilities. In this case, the lessee would need to disclose this effect as a non-cash change in lease liabilities in the statement of cash flows.

Accounting for lease concessions within the modification framework

If a lessee does not elect to account for COVID-19 rent concessions using the expedient outlined in the May 2020 amendment to IFRS 16 or is not eligible to apply it, a lessee would account for any adjustments to rent payments as a modification in accordance with the applicable guidance in IFRS 16. After determining that a separate lease is not required as a result of a modification, the lessee remeasures the lease liability and ROU asset to reflect the new consideration using an updated discount rate as of the effective date of the modification.

Summary

As a result of COVID-19, lessors may be willing to grant rent concessions that work for both parties. To ease the burden of having to account for those concessions as lease modifications within the IFRS 16 modification framework, the IASB has amended IFRS 16 to add an optional expedient for lessees to account for these concessions as changes that are not modifications. The practical expedient is only available to lessees and specifically applies to rent concessions that impact lease payments that were originally due on or before June 30, 2021. If a lessee elects the practical expedient outlined under the IFRS 16 amendment for COVID rent concessions, the lessee must disclose when and how the expedient was used, as well as the accounting effects of applying the expedient to the COVID-19 rent concessions.