COVID-19 Background

The current coronavirus pandemic is impacting countries all over the world. International and domestic economies have all been hit hard by the virus. Businesses across all industries and sizes are facing challenges to their sales, operations, and supply chains. As businesses are facing cash flow, revenue, and longevity concerns, their ability to meet upcoming financial obligations is coming into question.

Specifically, as companies monitor cash flow and look to assets that may be under-used during this pandemic period, entities are reviewing their lease commitments. Going through a legal battle over non-payment of rent is not an ideal situation for either party in this stressful and difficult time. A renegotiation of lease terms is a possibility. However, as a lease is a legally binding contract, the lessee and the lessor must agree on any changes to the lease agreement.

Changes to lease payments under COVID-19

As businesses renegotiate their existing agreements, lessee and lessors will attempt to find new terms that are agreeable for both parties. Some examples of possible rent concessions include rent forgiveness, rent reductions, or a rent “credit”. Another scenario is the deferral of rent payments, with payment occurring at a later date.

Under ASC 840 or ASC 842, any of these scenarios may trigger a lease modification as there has been a change in the terms and conditions of the contract. Lease modifications occur when changes are made to the scope or consideration of the original terms and are agreed upon by both the lessee and lessor. A lessee remitting decreased payments to a lessor due to financial difficulties without prior agreement is not a lease amendment, and may cause the lessee to be in breach of the lease agreement. A change to a lease agreement or a concession is not effective until both parties agree to the adjusted contract.

The April 8, 2020, Financial Accounting Standards Board (FASB) meeting included a discussion of the impacts of COVID-19 on a company’s lease accounting. One of the topics discussed specifically related to concerns around how to account for lease concessions as a result of the current global pandemic.

The FASB has acknowledged that during this unprecedented time organizations may find it difficult to determine whether concessions provided to lessees are considered a lease modification. It is often costly, complex, and burdensome for entities to go through a large number of contracts quickly to determine whether the existing contracts provide enforceable rights and obligations for lease concessions, and if so, whether it is consistent with the original terms of the contract, or is a modification of the original lease.

The current guidance around lease modifications in ASC 840 and ASC 842 addresses lease changes that occur in the ordinary course of business, not changes that happen on a global scale, as a result of a financial crisis such as COVID-19. Therefore, in order to provide relief from the complexities of lease modification accounting the FASB has provided an approach that serves as an electable alternative to modifying the lease. This approach permits entities to treat lease concessions as a direct result of the COVID-19 pandemic as if they existed in the original contract, and are therefore not required to be treated as a lease modification. Instead, companies can elect to treat these new enforceable rights and obligations as if they existed in the original contract and account for the concessions in the current period. For more information, refer to the FASB’s Staff Q&A on accounting for leases during COVID-19.

Instead of going through each lease individually to determine whether it is a modification under the frameworks of ASC 840 and 842, companies can choose, as an accounting policy election, not to perform this evaluation. This election can be applied enterprise-wide or for leases with similar characteristics or circumstances (i.e. class of assets or similar types of concessions in similar lease arrangements).

The FASB has indicated that this election is only available for COVID-19 lease concessions that result in the total consideration required by the contract being substantially the same as, or less than, the total consideration originally required by the contract. Since the term “substantially the same” was not explicitly defined by the FASB, it is expected that companies will apply judgment when determining whether this election is applicable to their lease concessions.

For example, if the parties agree to defer the rental payments from April 2020 to be due in November 2020 or to a concession of 25% of the rental payment due for April 2020, the election can be applied. However, if rent concessions coincide with a significant increase in the lease term, (i.e. the concession’s impact is NOT substantially the same as the original lease payments) this must be recognized as a modification under ASC 842. For example, if as part of offering rent deferrals or reductions, the lessor requires the lessee to extend the lease term by two years, this would not qualify for the COVID-19 election. This is because, while payments in certain months may have decreased, the total payments for the lease term have increased substantially with the addition of two years.

It’s also important to note that any change to a lease agreement, whether accounted for as a modification using the rent concession election or not, must be agreed upon by both parties. Any waiver from the payments outlined in the lease agreement NOT agreed to by both the lessee and the lessor, such as “short-pays,” are not eligible for this election.

Due to the economic volatility, the Federal Reserve has significantly dropped interest rates as part of an emergency action plan to help protect the economy from further COVID-19 impact by lowering borrowing costs as much as possible. Because of the significant drops in borrowing rates, electing to apply the FASB’s relief guidance which avoids the re-assessment of discount rates required under modification accounting, also provides benefit to a company’s balance sheet.

Applying a lease modification requires a remeasurement of the lease liability and right-of-use (ROU) asset using the discount rate at the modification date. If using potentially lower borrowing rates for the remeasurement, companies may end up with a higher liability calculation at the time of the modification than they had before. This occurs because although payments have decreased, the discount rate also decreased resulting in a higher obligation. However, electing the FASB’s relief guidance for COVID-19 related lease concessions does not require updating the discount rate. Therefore, the lease liability and ROU asset would not increase due to a change in the interest rate.

Accounting for COVID-19 lease concessions

Deferral of payments

Some lease concessions may include a deferral of payments until a later date, with no changes to the total consideration in the original lease and no change to the cash flows over the lease term.

Once a lessee has decided to utilize the FASB’s rent concession election, LeaseQuery recommends one of the three approaches outlined below, depending on whether the concession is a rent deferral or a rent reduction.

Approach 1: Short-term payable (No remeasurement)

In the month(s) of the rent deferral, the lessee would utilize a short term payable or clearing account to record the portion of the payment that is deferred to a later date. When the payments are actually made, the short-term payable or clearing account is relieved. Under this approach, the lessee does not need to remeasure the ROU asset or lease liability and continues to account for the ROU asset and lease liability using the rights and obligations of the original lease (i.e. there is no change to the amortization schedule).

As an example, assume a lease with payments of $1,000 monthly has one month of lease payments deferred. Using Approach 1 for payment deferrals, the entries for the lessee look like this:

As noted above, the lessee would continue to record changes in the lease liability and ROU asset based upon the original amortization schedule.

The overall benefit of this approach is there are no changes to a company’s recurring accounting and no recalculation or remeasurement of the ROU asset or lease liability. This approach is ideal for arrangements in which the lessee receives an interest-free rent deferral, payable at a later date, with no other changes made to the lease agreement.

Approach 2: Negative variable lease payments

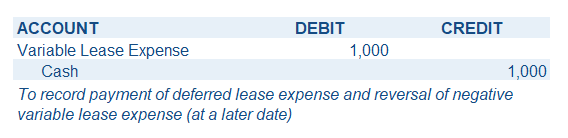

This second approach allows for the lease concession to be treated as a negative variable lease payment. The deferred payments are recorded as negative lease expense in the months the rent payments would have been due per the original lease agreement. There would be no impact on the ROU asset, lease liability or the lessee’s amortization schedule. When the payment is made at a later date, the lessee debits variable lease expense, effectively reversing the negative variable lease expense that was previously booked. This treatment keeps the total cash paid and expense recognized consistent with the original lease agreement., The timing of the expense recognition and cash payments is adjusted using the variable expense.

Let’s use the same scenario from Approach 1 to calculate Approach 2.. A lease requires monthly payments of $1,000 and one month of lease payments is deferred. Using Approach 2, the entries for the lessee would look like this:

This approach causes total lease expense during the deferred periods to be lower by the deferred amount and higher by the deferred amount when the payments are made. Because the lease liability is reduced based on the existing amortization schedule, the lease liability presented will be less than the amount that the lessee is legally obligated to pay until the payment is made. This is because the liability is being reduced in the periods of deferral but no payments are being made.

Approach 3: Remeasurement consistent with resolving a contingency

This approach, unlike Approaches 1 and 2, requires remeasurement of the lease liability and is applicable under ASC 842. This method treats the concession as an option the lessee is entitled to under the original lease contract. Therefore the new timing of the rent payments is accounted for as a resolution of a contingency specified in the original lease. The lessee remeasures the lease liability using the remaining lease payments but does not update the discount rate used in the present value calculation. Additionally, the lessee is not required to reassess the classification of the lease and will also not reassess the lease term or a lessee purchase option. The lease liability is adjusted to reflect any change in the carrying value based on the remeasurement, and the lessee makes a corresponding adjustment to the ROU asset.

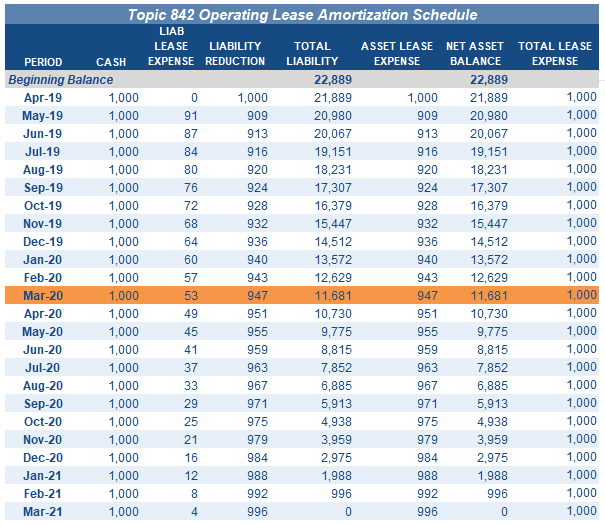

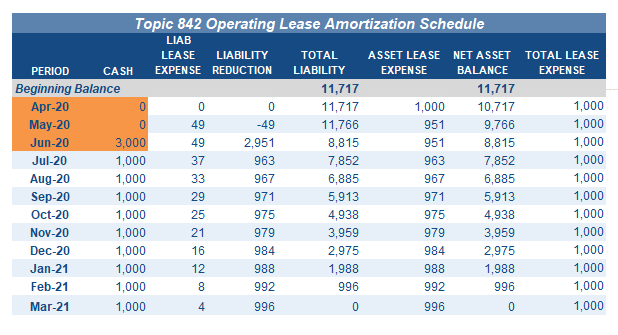

As an example, assume the same facts as above. The original lease is a 2 year lease starting April 1, 2019, with $1,000 monthly payments, paid in advance at the beginning of the month, with a discount rate of 5%. Using the present value calculator tool, the initial lease liability and ROU asset are $22,889. At the end of the first year, the carrying value of the lease liability and ROU asset are $11,681.

As of April 1, 2020, due to the COVID-19 pandemic 2 months of lease payments are deferred to the next month ($0 due for April and May, and $3,000 due in June). By using the present value calculator again to measure the lease liability using the same 5% discount rate and the updated payment timing, the remeasured lease liability comes to $11,717.

The difference between the new lease liability and the lease liability before the lease concessions were granted ($11,717 – $11,681 = $36) is recorded and the ROU asset is adjusted by the same amount. This is done by the following entry:

Payment reductions

Approach 1: Short-term payable

Approach 1 is not available for rent reductions. It is only available as an option if the changes within the lease concession are timing differences, not if a true rent reduction occurs.

Approach 2: Negative variable lease payments

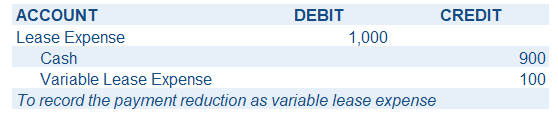

As discussed above, the second approach allows for the lease concession to be treated as a negative variable lease payment. During the periods of rent reduction, the reduction is recorded as negative lease expense in the month when the rent payment would have been due per the original lease agreement. There would be no impact on the ROU asset or lease liability, as the lessee would continue to record lease amortization in the correct periods.

In contrast to a rent deferral, because the reduction will not be paid at a later date, there is no reversal of the negative lease expense previously booked.

Let’s assume a lease agreement has payments of $1,000 monthly and one month’s lease payment was reduced to $900. Using Approach 2, the entries for the lessee would look like this:

This treatment results in the reduction of the lease liability and lease asset being consistent with the amount on the original lease amortization schedule, but reduces the total expense recognized in the general ledger over the lease term. The reduction to the lessee’s expense occurs in the period of rent reduction through the variable rent expense.

Approach 3: Remeasurement consistent with resolving a contingency

Approach 3 treats reductions to payments as a resolution of a contingency specified in the original lease. The lessee is not required to reassess the classification of the lease, or the lease term and purchase options. However, the lessee adjusts the value of the lease asset and lease liability to the present value of the remaining lease payments using the original discount rate.

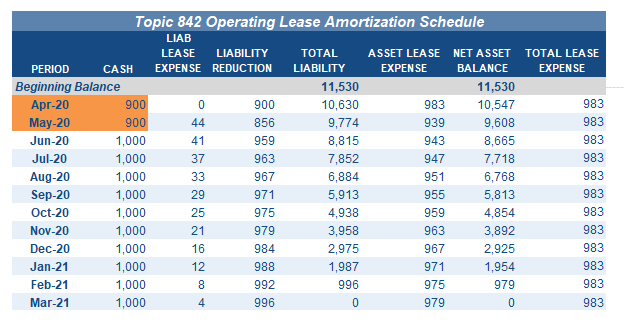

As an example, assume the same facts as above. The original lease was a 2 year lease with $1,000 monthly payments, and payments are made in advance at the beginning of the month, with a discount rate of 5%. Using the present value calculator tool, the initial lease liability and ROU asset are $22,889. At the end of year 1, the carrying value of the lease liability and ROU asset is $11,681. (Refer to the amortization table under Approach 3 for deferred payments for a full example of the amortization of the initial lease liability and ROU asset.)

At the beginning of April 2020, the lessee and lessor agree on a concession as a result of COVID-19 to reduce lease payments for 2 months to $900/month. By using the present value calculator again and remeasuring the lease liability with the newly reduced lease payments, the new lease liability is $11,530.

The difference between the new lease liability and the lease liability before the lease concessions were granted ($11,530 – $11,681 = -$151) is recorded, and the ROU asset is adjusted by the same amount. This is done by the following entry:

Summary

Multiple scenarios exist where a lessor and lessee can amend a lease agreement to offer relief as a result of COVID-19. To ease the burden of accounting for these changes within the current lease accounting guidance, FASB offers an electable alternative to recognize the financial impact of the concessions in the current period. We have presented three approaches for deferred payments and two approaches for payment reductions. If any material concessions are granted to the lessee, both the lessee and the lessor should disclose the accounting effects of the transactions in order to provide transparency in regards to the effects of COVID-19.

Accounting for lease concessions within the modification framework

If a company does not make an accounting policy election (either on an entity-wide basis or by asset-class) to account for COVID-19 rent concessions using the FASB’s relief guidance, entities would account for any adjustments to rent payments as a modification in accordance within its applicable lease guidance of ASC 840 or ASC 842. A lease modification includes remeasuring the lease liability and ROU asset to reflect the new consideration, re-evaluation of the discount rate, and re-assessment of the lease classification on the modification date.

In evaluating cash flow and resource needs, a company may realize that they no longer need all of the leased asset. As a result, a company may negotiate for full or partial termination of a lease. If the lessee has determined that they will no longer be using a portion of the leased asset, a partial termination has occurred. If you have a partial termination, you can review that accounting here. A full explanation and examples of accounting for lease terminations can be found here.

While the discussion in this article focuses on examples from the lessee’s perspective, the FASB has stated that lessors can also utilize the elections available for lease concessions granted due to COVID-19.